In late 2018 / early 2019, we spoke to 50+ participants within the Indian EV ecosystem and published our views on its evolution in two articles – Part1 and Part 2. Since then, a lot has changed. Most initial experiments have failed. Numerous start-ups (and some incumbents) have launched substandard products that were mere assembly of cheap Chinese kits and poor quality batteries. The most touted company – Ather – built a good product but has not been successful in building a product for the price-utility needs of the Indian market. Subsidies and regulations have been an integral part of EV adoption across the globe, but the Indian Government has been disappointing on this front. There have been delays and policy flip flops, and whatever has been done is too little to catalyze anything. Indian automobile industry has had tough times over the last year and COVID has further pushed it towards the grave.

So does that mean EVs for India are dead?

We do not think so. The rise of EVs is inevitable. Crowded cities, worst pollution globally, dropping Li-Ion prices – all create a perfect storm for India to adopt EVs. It will be the biggest disruption for our automotive industry after the creation of Maruti in 1980.

Over the last 12 months, we have spoken to 150+ EV ecosystem participants and are presenting our updated view across three articles (1) Opportunities for new OEMs, (2) Opportunities within the battery ecosystem, and (3) Opportunities in energy distribution.

—————————————————————————–

History suggests that creation of a new automotive OEM is next to impossible. Incumbents always win this war due to the long product development cycles, high investments in supply chain, distribution and service networks, and the long duration to build brands. But then, never have we faced such a massive disruption in the automotive space that challenges all the assumptions.

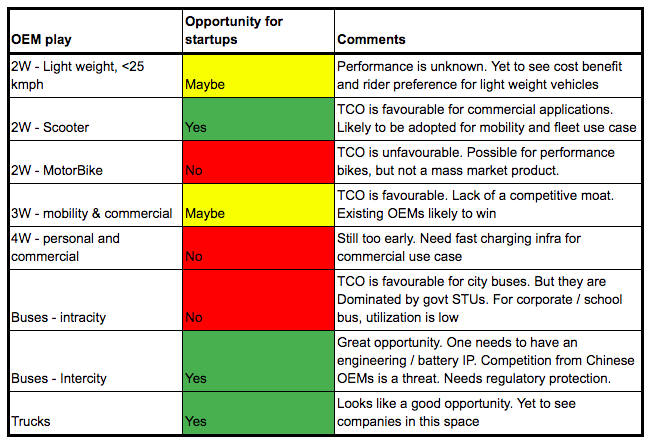

We also believe that most of the EV opportunity will be grabbed by incumbents. However, most large automobile companies are struggling with innovation inertia and creative disruption, and have at best doodled with new EV solutions; giving startups a window of opportunity to capture sufficient market share to become serious players in their own right. We believe there is still an opportunity to build a new OEM in 2 spaces:

- A scooter built for commercial usage/fleets

- Intercity bus/ trucks

A commercial EV scooter designed for India can be the potential winner

18 months back, we were very bullish on an EV scooter as one of the best opportunities within the EV landscape, and our thesis has not changed. India is the world’s largest 2W market, ~7x in annual volume sales compared to passenger cars.

Why commercial? Given the higher upfront cost and lower running costs of an EV, commercial applications are better suited given the higher daily usage leading to faster recovery of additional upfront capital.

Why scooters and not mobikes? We believe that fleet owners, e.g. Vogo, Bounce, Yulu etc., are likely to to be the early adopters of EVs, and pretty much all of them use only scooters given their appeal with both men and women, and gearless systems leading to lower mishandling. Delivery fleets (e.g. with Swiggy, Delhivery, Loadshare, etc.) are a larger segment and predominantly motorcycles, but the asset owner there is the individual driver, and we believe individuals will shy away from buying EVs in the initial years as the risk appetite of this socioeconomic class is limited until these vehicles are proven.

Favourable TCO for commercial applications

Fuel costs for an electric scooter are 80% lower than their ICE counterparts. A higher utilization of the scooter will lead to higher fuel savings. Even though EVs are getting cheaper every year, they still cost 60-80% higher than their ICE counterparts. Whether savings on the fuel will be enough to cover the extra cost of purchase depends on the utilization of the vehicle.

Below is a comparison of the total cost of ownership (TCO) for a vehicle for private use having utilization of 25 km/day with one for commercial use having utilization of 100 km/day. We can see that over a 5 year period, owning an electric scooter for a personal use case is roughly 20% costlier; while the same is 25% cheaper for commercial usage.

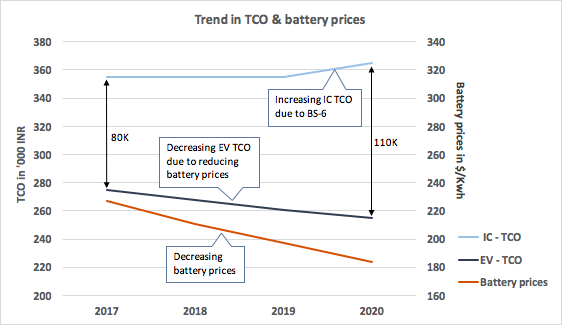

The business case for EVs further intensifies with the introduction of BS-6 engines and due to the continuous reduction in battery prices. BS-6 will increase the ICE scooter prices by 15%. Whereas in the last 3 years, battery prices have reduced by 18% resulting in 35% increase in the difference between electric and ICE TCO (for a 100 km/day utilization).

Indigenized design required for consistent performance

Despite favourable TCO, electric scooters, as they are available today, are not ready to deploy for commercial use.

“We have tried most electric scooters available in the country. Almost all of them break down within 6 months. As of today, it’s not an economical option for us” – says the founder of a large scooter fleet operator we spoke to.

There are dozens of companies selling electric scooters, but most of them rely on direct or indirect imports from China, with very minimal value addition. Those scooters, when put through rough and shared use under harsh Indian conditions, have a significantly lower lifespan. This defeats the entire TCO case for EVs because the total utilization over the lifetime is low.

We believe that companies that are designing, testing and manufacturing the vehicle grounds up – one that is built for India and suitable for rugged commercial use cases – stand a chance to win this market.

We find it a little surprising that despite the years of experimentation with EVs in India, there has not been a single good EV scooter yet. Ather created a good but over-engineered product. A scooter is a utility vehicle and not a status symbol, and hence buying sentiment will be driven by price, durability and utility. Consequently, Ather, in our opinion, has failed to achieve product-market fit. Our view is that there is still time for a team with strong engineering, quality and cost orientation capabilities to build an EV scooter and achieve a certain scale before the incumbents get their act together on innovation.

Building a good EV scooter is non-trivial as the form factor imposes size, shape and density implications on the battery, which is the heart of the vehicle. This will require the OEM to have strong battery skills, which we find are still in short supply. Claims of existing OEMs are mostly misplaced on this front. Scooter batteries cannot be liquid-cooled, and with bumpier Indian roads, both the thermal and mechanical tolerances require strong engineering skills.

An intercity electric bus (or truck) with engineering IP stands a chance

Buses often travel a few hundred kms in a day and need large battery packs to deliver that range. Ample space in these vehicles makes it possible to have liquid-cooled battery packs that not only provide higher range for a given amount of power, but also have longer battery life.

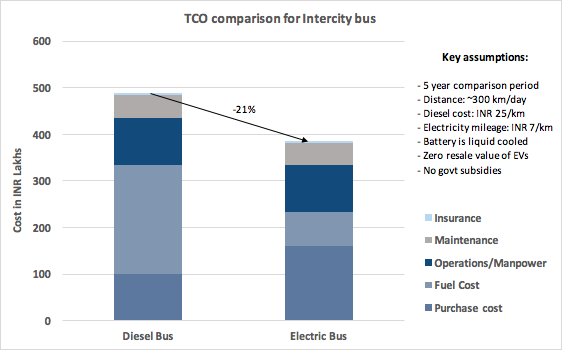

We are already seeing good penetration of electric buses in the intracity segment where most of the buses are owned by the state transport units (STUs). However, intercity transport, which is dominated by private players, is a more lucrative opportunity. An intercity bus usually travels on defined routes, doesn’t need a large charging network and can manage with just 2 or 3 charging points; at the source, the destination & maybe somewhere midway.

For a bus traveling an average of 400 kms/day, fuel cost accounts for 50% of its Total Cost of Ownership (TCO). Going electric can reduce its fuel cost by 70%, from INR 25-30/km to INR 7-8/km. Even though a Volvo equivalent electric bus costs INR 1.6 Cr, in comparison with INR 1 Cr for the diesel bus, the TCO for an electric bus is still lower due to much higher fuel savings over its lifetime.

China dominates the global electric bus market with 99% market share. Many Chinese Electric bus OEMs like BYD, Foton & Skywell are entering the Indian market through partnerships. However, Chinese players might find it difficult to compete in the short run due to investment restrictions and the inclination of the government to protect local industry. But in the long run, Indian companies starting in this segment need to build a compelling advantage over the Chinese players.

We believe that a similar opportunity will exist in the intercity trucking space as well. Truck logistics is a ~$100B market, with intercity segment as the dominant part. Economics for this segment is very similar to intercity buses. Even though we have seen very little action in this space yet, we believe that there is opportunity for new players in this space.

Incumbent OEMs likely to win the 3-wheeler market

Ironically, most of the real EV activity in India so far has been in 3Ws – India has more than 1.5M E-rickshaws – but we are not bullish on a new OEM in this space. While the argument for building an indigenized 3-wheeler (3W) carries weight, it is hard to build a meaningfully differentiated vehicle. Space and battery size are not big constraints for a 3W as there is enough space below the passenger seat. Instead of the product, brand & distribution capability are likely to play a bigger role in winning this market. Therefore, incumbents are more likely to dominate the 3W market.

We are excited to see how the OEM space will unfold for EVs. We will discuss the opportunities in the battery space in the next part. Meanwhile, if you are enthusiastic about EVs and keen to have a brainstorming session, feel free to drop a note at naman@stellarisvp.com